A tax-free savings account (TFSA) is like a bottle of red wine – it gets better with age. Compound interest and yearly contribution allowances enhance its benefits with time. Not sure what those are? Just keep reading. We’ll teach you the ins and outs of TFSAs, how they’re are useful for almost any financial plan, and 5 quick tips you need to know to make the most out of your own TFSA.

What is a TFSA?

A tax-free savings account, or a TFSA, is a government program for anyone over the age of 18 to save and invest their money tax-free. However, you can’t just deposit as much money as you want into a TFSA. There are contribution limits. And every year the government lets us know how much money we can contribute. The magic number for 2023 is $6,500. The good part is that if you didn’t deposit anything into your TFSA in 2022, you can carry your contribution room forward. Don’t worry if it sounds complicated, we’ll break it all down for you.

Tip #1: Know your contribution limit

Everyone’s contribution limit is different. And it’s critical that you only deposit how much you’re allowed. Why? Because the government will tax you 1% every month on the amount you over-contribute. For once, it doesn’t pay to be an overachiever.

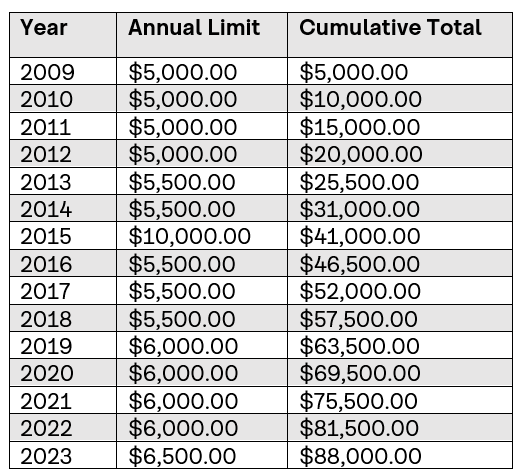

Before you ask, “So, what’s my contribution room?” here is a handy general contribution limit chart.

Basically, if you were over the age of 18 in 2009 and you’ve never deposited a single penny into your TFSA, you can deposit up to $88,000 in 2023.

Your contribution room also carries forward from one year to the next. So, if you only deposited $2,500 in your TFSA in 2022, you can still deposit the remaining $3,500 any time in the future.

Just remember, before you start depositing money into your TFSA, double-check your limit on the CRA website or, give us a shout if you have more questions.

Tip #2: Automate saving

We’re not talking robotics. We’re talking scheduled recurring transfers. Every two weeks, around payday, schedule a recurring transfer to your TFSA. You can choose the date and the amount—be realistic with your budget. Automating the act of saving will help you keep within your contribution room and stick to your savings plan. If you don’t see the money, you can’t spend it. Just like other paycheque deductions, you’ll hardly miss it when it’s gone.

Tip #3: Think long-term

A TFSA should be a pit-stop for your money. Think of it as a metaphorical SkyTrain station because anyone who goes to a SkyTrain station just wants to hop onto a train and end up somewhere else. So does the balance in your TFSA.

A TFSA is a perfect vehicle for your investments. You can keep the money just in the TFSA but really, you should invest your balance into a variety of investment solutions such as (but not limited to) GICs, mutual funds, and ETFs. Your money is not working as hard as it should if it’s just accruing interest at the default TFSA rate set by your bank.

Tip #4: What tax-free really means

When most people think tax-free, they think tax-free like RRSPs. If you deposit $10,000 into an RRSP, when it’s time to file taxes, it’ll lower your annual income by $10,000. That means you won’t pay taxes on that $10,000.

Spoiler alert: TFSAs don’t work like that.

Tax-free means you don’t pay any taxes on the interest you accumulate in your TFSA. Let’s say you invest $10,000 through your TFSA and earn $5,000 in returns. Since the investment was through your TFSA, you don’t have to pay any taxes on the $5,000.

But you will have to tell us how you earned a 50% return on your investment. Because that is amazing and you are hired.

If you want to check out how much tax you’ll save on the interest you earn through a TFSA, check out our nifty TFSA Calculator.

Tip #5: You can withdraw your funds—tax-free

Yes, you read that right. Unlike RRSPs, you don’t pay taxes on the money you withdraw from your TFSA. Let’s keep daydreaming about that 50% return and use it in another example:

If you’ve made a return of $5,000 from your TFSA investments but all of a sudden your washer and dryer break—coincidentally at the same time, because that’s how life seems to work—you can simply withdraw that $5,000 from your TFSA to buy new appliances without any tax penalties or implications.

TFSAs are a flexible financial tool for us to benefit from. You can deposit more money into it every year, generate tax-free interest on your investment, and withdraw it whenever you want without being taxed. If you want to open a TFSA, schedule automated transfer to your savings, or need investment help, talk to us today.